VWAP Calculator

The VWAP Calculator defines a security's average price weighted by volume, that is, the volume weighted average price (VWAP).

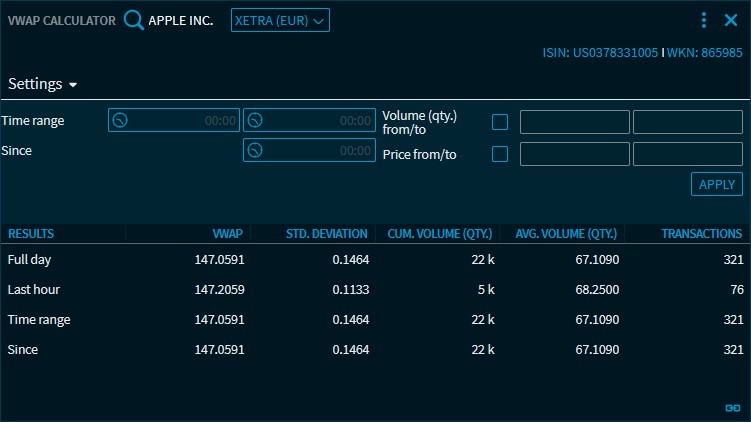

In addition to the VWAP, you find key figures such as standard deviation, cumulative and average volume as well as the number of transactions.

In the table, the results are shown for the following periods: "Full day", "Last hour", "Time range" and "Since".

In addition to the standard elements of the widget, you find the following elements in the "VWAP Calculator" widget:

Field | Description |

|---|---|

Settings | Expand or reduce the settings area. |

Period | In the "Time range" area, enter a start and/or end time or enter a start time in the "Since" field for the analysis up to the current moment. |

Volume (qty.) | To filter the data by volume, select this checkbox and enter a minimum and/or maximum value for the quantity in the corresponding input fields. |

Price | To filter the data by certain prices, select this checkbox and enter a minimum and maximum value in the corresponding input fields. |

Apply | After specifying your settings, click this button to recalculate the key figures. |

The VWAP calculation applies only to the current trading day, historical data is not available.

In the Widget Gallery, you find the "VWAP Calculator" widget in the "Calculator" section of the widgets for shares, bonds and certificates.